With chronic wounds and trauma cases on the rise, demand for advanced treatments such as CAMPs (cellular, acellular, and matrix-like products) is growing fast. At the same time, insurers are tightening reimbursement and favoring products backed by strong clinical evidence. As regulatory pathways remain fragmented, the CAMPs market is becoming a proving ground for innovation. Advances in tissue engineering, biomaterials, and surgical techniques are accelerating uptake. Yet growth brings its own set of challenges. Companies must navigate complex approvals, shifting coverage policies, and rising development costs.

The development of CAMPs, including allografts, xenografts, and synthetic substitutes, marks an important shift in wound care. These products are now a meaningful part of advanced treatment for hard-to-heal wounds, but their use still depends heavily on reimbursement, care setting, and physician choice. That makes the category attractive, but also exposed to policy changes and pricing pressure.

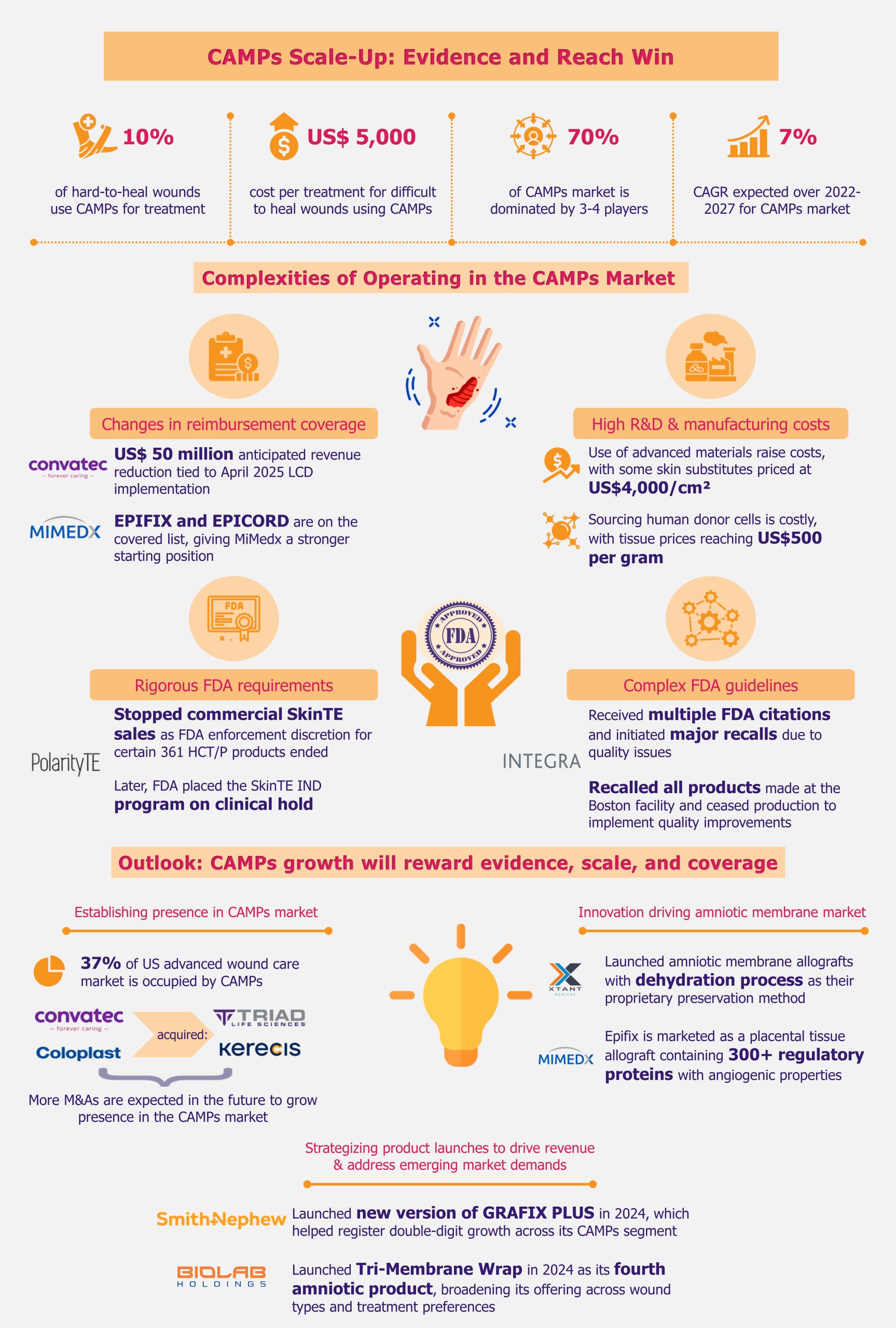

The CAMPs market presents significant growth opportunities, but players face persistent challenges that limit profitability and scale. Uncertainty around reimbursement and frequent changes to coverage disrupt planning and access. At the same time, navigating complex, costly regulatory pathways slows product launches and deters new entrants. High R&D and manufacturing costs add to the burden, making market success harder to sustain.

Reimbursement changes are reshaping how CAMPs companies compete

The CAMPs market faces uncertainty as Medicare Administrative Contractors tighten coverage rules. The final LCDs issued in late 2024 narrowed reimbursement for DFU and VLU treatment to a much shorter list of products supported by stronger published evidence. As of February 2025, those changes were set to take effect on April 13, 2025, after a short delay.

Under the final LCD approach, companies with stronger published evidence would be more likely to keep access to high-volume DFU and VLU use cases. That could create a second-order advantage for larger players. They would be better placed to keep funding trials, defend coverage, and shift sales resources toward the care settings still worth chasing.

Additionally, smaller players may struggle to market their products. That is especially true for companies with limited product ranges selling to wound care centers, podiatric offices, and vascular surgeons. These providers primarily treat diabetic foot ulcers (DFUs) and venous leg ulcers (VLUs), which are the main focus of updated LCDs. Providers are unlikely to accept those products for DFU and VLU, even if they remain suitable for trauma wounds.

“Smaller companies carrying 1-2 products would get impacted. The regulations are applicable to the treatment of DFUs and VLUs. So smaller companies will have a hard time selling related products in podiatric offices and vascular practices. Those providers see several VLU cases. Selling to wound care centers dealing with DFU and VLU will be difficult, too. But the products could still be used for other wound types, such as trauma or surgical wounds. However, DFU and VLU account for a very large percentage of business, which they will lose.” – Senior Tissue Regeneration Specialist, Organogenesis

Even larger CAMPs players remain exposed to LCD risk

Policy changes will affect even larger players, such as Convatec. Based on the implementation of the LCDs in April 2025, Convatec said it expected about a US$50 million reduction in InnovaMatrix revenue. This is a noticeable change. Medicare DFU and VLU sales made up about three-quarters of InnovaMatrix sales in 2024. That shows how exposed even scaled players can be to reimbursement shifts.

On the other hand, the tougher evidence focus could benefit some established players such as MiMedx. EPIFIX and EPICORD are on the covered list under the LCD approach, while products such as EPIEFFECT are not. That gives MiMedx a better starting position than many smaller rivals. More broadly, players with covered products and stronger evidence are entering 2025 with a clearer advantage. The same is true for companies with enough cash to keep investing.

“The larger companies are still running RCTs for some of the products. So that way, they can expand their portfolio to be used particularly for DFU after the LCDs are implemented. Priority will be on gathering clinical evidence. Also, larger companies may strengthen their salesforce to reach wound centers, private offices, and ORs. There are clinical trials underway to add Epieffect to the LCD list. Delays in LCD implementation benefit companies running ongoing clinical trials.” – Senior Tissue Regeneration Specialist, Organogenesis

Cash reserves and partnerships can cushion reimbursement shocks

Since the latest LCDs were proposed, several industry players have moved to strengthen their market position through licensing deals and operational investments. MiMedx, for example, ended FY2024 with US$104 million in cash reserves. That gives it more room than smaller rivals to absorb policy shifts, keep funding studies, and defend its share.

CAMPs Scale-Up Turns Wound Care into a Test of Evidence and Reach by EOS Implicium

In 2024, StimLabs signed an exclusive national distribution agreement with Geistlich to commercialize Derma-Gide, a porcine-derived matrix. Although none of StimLabs’ own products are covered under the current LCD list, Derma-Gide is approved. The partnership allows StimLabs to enter the xenografts segment of wound care. It gives providers a covered option and helps the company gain a stronger foothold in the CAMPs market.

Smaller CAMPs players face steep barriers in a tightly controlled market

Navigating the FDA approval process remains a major challenge for industry players. The pathway is long, costly, and demanding, adding to development timelines and delaying market entry.

FDA approval remains complex, costly, and hard to navigate

Companies must meet a long list of pre-market and compliance requirements, but the pathway is not the same for every CAMP. Some products may qualify as HCT/Ps under section 361 if they meet FDA criteria. Others may need 510(k), PMA, or biologic review depending on composition, processing, and claims. That complexity adds cost, slows launches, and raises the risk of choosing the wrong regulatory path early.

Players such as RegenETP, formerly PolarityTE, have faced serious regulatory setbacks. In 2021, the company said it would stop commercial SkinTE sales as the FDA enforcement discretion for certain 361 HCT/P products ended. The agency later placed the SkinTE IND program on clinical hold over chemistry, manufacturing, and controls issues. For companies tied closely to one lead product, that kind of setback can hit revenue quickly. It can also pull management attention away from growth.

Unclear FDA rules are driving delays and strategic missteps

The bigger problem is not just that the FDA pathway is complex, but also how that complexity changes business models. When approvals are slow, costly, and hard to predict, some companies avoid building every product in-house. Instead, they widen their portfolio through distribution or partnerships. Organogenesis is one example of how companies use that approach to keep their salesforce active without carrying the full R&D burden across every product.

“Organogenesis only has four products with pre-market approval. The approval process is long, rigorous, and complicated. R&D and manufacturing costs are very high. A lot of companies don’t want to go through all of that, so we only have four approved products. However, we sell products that are owned by different companies, such as Cygnus Dual and Via Matrix. We’re not investing money in R&D and production of these two products, but it allows our salesforce to sell more products.” – Senior Tissue Regeneration Specialist, Organogenesis

Clinical expectations for CAMPs are still not fully standardized across product types. That leaves companies with uncertainty around study design, endpoints, and evidence depth. That uncertainty can weaken regulatory planning, delay programs, and raise the risk of later quality problems, recalls, or manufacturing disruption.

Regulatory missteps can trigger recalls, shutdowns, and revenue loss

Integra LifeSciences offers a recent example. Between 2023 and 2024, the company received multiple FDA citations and initiated major recalls due to quality issues. In 2023 alone, the company had to recall all products made at its Boston facility over the previous five years. It also had to cease production to implement quality improvements. The FDA also cited Integra for good manufacturing practice violations. The issues affected products in wound care, soft tissue repair, and reconstructive surgery. This showcases the scale of impact that the FDA’s scrutiny and monitoring can have on players, from production shutdowns to revenue loss to severe erosion of both top and bottom lines. The consequences could be even more severe for smaller players with limited resources.

High R&D and manufacturing costs are straining CAMPs players

Developing CAMPs demands heavy investment in R&D and manufacturing. Companies must fund cellular engineering, biocompatibility testing, and clinical trials. Manufacturing CAMPs is an intricate process requiring specialized production facilities that meet strict regulatory and quality standards. The use of advanced materials and technologies drives costs even higher, with some skin substitutes costing US$4,000 per square cm.

“The R&D and manufacturing costs of operating in this industry are very high. Smaller companies survive by focusing on products with a higher average selling price (ASP). So, catering to a 7*7 wound reimbursed at US$ 3,000 sq cm is much more beneficial than the one reimbursed at US$150 sq cm. It’s much easier because you’re still only handling one tissue, but the return is higher. Higher reimbursement significantly improves margins and reduces the relative administrative burden.” – Senior Account Executive, MiMedx

Companies such as Organogenesis have invested heavily in manufacturing, commercial operations, and R&D. Its facilities span about 300,000 sq ft, 43,850 sq ft, and 122,000 sq ft. In 2024, Organogenesis increased its R&D expense by 13% year over year. It did so as it expanded clinical research for pipeline products and studies tied to regulatory approvals.

Donor sourcing costs keep CAMPs’ margins volatile

Sourcing human donor cells is a major cost driver for CAMPs companies, with human tissue priced as high as US$500 per gram. These high costs reflect the complexity of the procurement process. Tissue type, processing methods, and other variables further influence the final price. Quality can also vary significantly, creating risks for manufacturers. Amniotic fluid has been contaminated in several cases despite strict screening protocols. Such lapses can lead to contaminated batches, product failures, costly recalls, and a loss of trust among clinicians.

From a broader view, while high ASPs (above US$3,000/cm²) can deliver strong gross margins, manufacturers still face volatile net returns. Donor sourcing is expensive, quality assessment sometimes fails, and batch yields can be low. As a result, profitability often depends less on pricing and more on scalable production and reliable, predictable reimbursement.

EOS Implic-Action: CAMPs growth will reward evidence, scale, and coverage

As regulatory pressure increases, the CAMPs market is becoming less of a pure growth story and more of a test of scale, evidence, and commercial discipline. Companies with covered products, broader portfolios, and enough capital are better placed to hold share. That matters as reimbursement tightens and acquisitions continue.

A strong CAMPs position is becoming essential in advanced wound care

Over the past decade, the CAMPs market has transformed significantly as new technologies and products entered the field. However, it has also faced instability, particularly due to shifting reimbursement policies across different care settings. Despite numerous challenges, the CAMPs market grew at a strong CAGR of 23% over 2017-2022. From 2022 to 2027, it is forecast to grow at a moderate 7% CAGR. While this growth rate does not match the previous stellar performance, it still signals strong momentum.

In Q3 2023, CAMPs alone accounted for 37% of the US advanced wound care market. That put them ahead of categories such as negative pressure wound therapy and advanced dressings. Eight out of ten leading advanced wound companies in the USA are active in the CAMPs market. Recent acquisitions reflect a clear shift among advanced dressing companies. Convatec bought Triad Life Sciences, and Coloplast acquired Kerecis. Both moves strengthened their foothold in CAMPs.

Related reading:

Advanced Wound Dressings Face Europe’s Price Test Despite Demand

LCD pressure could push weaker CAMPs players out of the market

“All companies are looking to grow and expand their portfolios. A lot of new players may also enter the market, but if changes to LCD are made, then you’re not going to see as many companies in this segment.

In the last five years, most companies have launched new products because Medicare reimbursement has been lucrative. That is especially true for high-ASP products. If LCDs are implemented, there will be a dramatic reduction in the number of companies that are operating, especially if that’s their only business model. Some companies are searching for ways to diversify into dressings or acquire products outside of CAMPs.” – Senior Tissue Regeneration Specialist, Organogenesis

Companies continue to invest in product innovation, but many are also expanding their reach through acquisitions. Players such as Organogenesis, Integra, MiMedx, and Smith+Nephew already control about 70% of the CAMPs market. Future acquisitions are likely to deepen this concentration, pushing the market further toward an oligopoly.

Consolidation is favoring scale, reach, and contracting power

This trend raises entry barriers for smaller players. As consolidation grows, providers and facilities often prefer companies with broader portfolios and stronger contracting support. They also value more reliable commercial coverage across care settings. Smaller firms may still win business through discounts or focused selling. But they have a harder time matching the reach and staying power of established players.

“The smaller players are typically companies that enter the marketplace carrying 1-2 different products. They often don’t have a big sales force similar to a large company, instead they hire independent contractors, who offer rebates and discounts to sell products. You’ll never find reputable larger companies offering rebates. That’s sometimes how they take our market share from us.” – Senior Tissue Regeneration Specialist, Organogenesis

“Smaller players are able to stay competitive by offering products that can give better reimbursement, with some products getting reimbursed at US$ 3,000 per sq cm. It is a huge revenue source for some providers, and they are eager to use the products. These companies mostly focus on private clinics instead of established hospitals.” – Senior Account Executive, MiMedx

Explore more analysis on EOS Implicium

Innovation is reshaping the crowded amniotic membrane segment

The amniotic membrane segment is one of the most active parts of the CAMPs market. But exact market-size estimates vary widely depending on which products and geographies are included. The more useful point is competitive behavior. Companies keep launching new amniotic products, refining preservation methods, and pushing product differentiation to win share in an increasingly crowded segment.

Manufacturers are exploring new preservation methods and highlighting distinct biological features to stand out. Some are also broadening beyond traditional amniotic products, including fish skin and other non-human tissue-based matrices, to reach wider parts of the market. At the same time, many still favor premium products that can support stronger reimbursement and margins.

“The amniotic membrane market is very competitive. Focus is on launching new types of grafts. We’ve seen fish skin, collagen, and amnion grafts. Players are constantly focusing on launching products with high ASP, so that reimbursement is higher. Doctors understand the revenue aspect and quickly gravitate to those higher ASP products.” – Senior Tissue Regeneration Specialist, Organogenesis

Shelf life and easier handling are becoming real selling points

As preservation techniques become a differentiator, Xtant Medical launched two amniotic membrane allografts in 2024, SimpliGraft and SimpliMax. Both use a proprietary dehydration process to remove moisture from the membrane. Better handling and longer shelf life can make products easier to store and use. They can also help Xtant place them across more care settings. That gives the company a practical commercial advantage, not just a technical one.

Beyond preservation methods, companies also compete in the crowded amniotic skin substitute market. They do so by highlighting unique biological characteristics as key differentiators. MiMedx promotes Epifix as a placental allograft with over 300 regulatory proteins, highlighting its anti-inflammatory and angiogenic effects. Organogenesis takes a different path with Affinity, which it positions as a fresh amniotic membrane allograft. Unlike dehydrated or cryopreserved alternatives, Affinity is marketed around retention of native tissue characteristics, including proteins and living cells. That gives Organogenesis a clearer differentiation in a crowded segment.

CAMPs players are refining product strategies to lift revenue

CAMPs players continue to invest in R&D to improve product safety, precision, and patient outcomes. Some of these efforts have led to clinical trials and product launches aimed at closing treatment gaps.

The growing focus is on innovation that drives both clinical value and financial performance. For instance, in 2024, Smith+Nephew launched GRAFIX PLUS. It is a new version of its CAMPs product aimed at the growing post-acute care market. The launch contributed to double-digit growth across its CAMPs segment.

BioLab Holdings is also expanding its amniotic portfolio. In 2024, it launched Tri-Membrane Wrap, its fourth amniotic product, giving the company a broader offering across wound types and treatment preferences. That kind of portfolio expansion can help companies win more physician attention without relying on a single flagship product.

Companies are leaning into niches to defend share

Other established players are refining their competitive strategies by carving out distinct niches. Organogenesis focuses on its proprietary living-cell technology to stay abreast of the competition. Smith+Nephew leverages its broad product portfolio and long-standing reputation. MiMedx has a very strong sales and contracting team, which has helped it build traction in outpatient settings.

“Organogenesis focuses on living cellular technology. We offer fresh living cellular grafts, and no other company offers those. So, we are in a class of our own. MiMedx has a very strong salesforce and contracting team, so they are very prominent in hospital outpatient centers. Smith+Nephew has been around for a long time. They’re a very reputable company and carry a little bit of everything. Every company has a niche of its own.” – Senior Tissue Regeneration Specialist, Organogenesis

“The larger companies leverage their relationships with providers and also have contracts with hospitals to cater to outpatient settings or ORs. Also, these companies are constantly launching new products or updating their portfolio to meet the requirements of different types of providers, private offices, or wound care centers. Larger players ensure that their product portfolio is balanced with products in all price ranges.” – Senior Account Executive, MiMedx

These tailored strategies do more than shape positioning. They affect which providers companies can reach, how well they can defend reimbursement, and how much pricing flexibility they have across care settings.

Reimbursement and care settings now shape CAMPs’product use

Reimbursement rules and care settings play a defining role in how providers use skin substitutes. As the LCDs move toward implementation, providers are likely to narrow usage. They will likely focus on products that meet both the evidence threshold and the economics of high-volume ulcer care. In response, several companies are investing to strengthen evidence and protect access. They are also trying to keep a foothold in the settings that matter most.

The CAMPs market faces real pressure from tighter reimbursement rules, regulatory complexity, and rising costs. Innovation still matters, but it will matter most for companies that can keep products covered, fund the evidence base, and sell across the care settings that drive volume. That gives larger, broader players a clearer path to defend share, while smaller firms with narrow portfolios will face a tougher road.