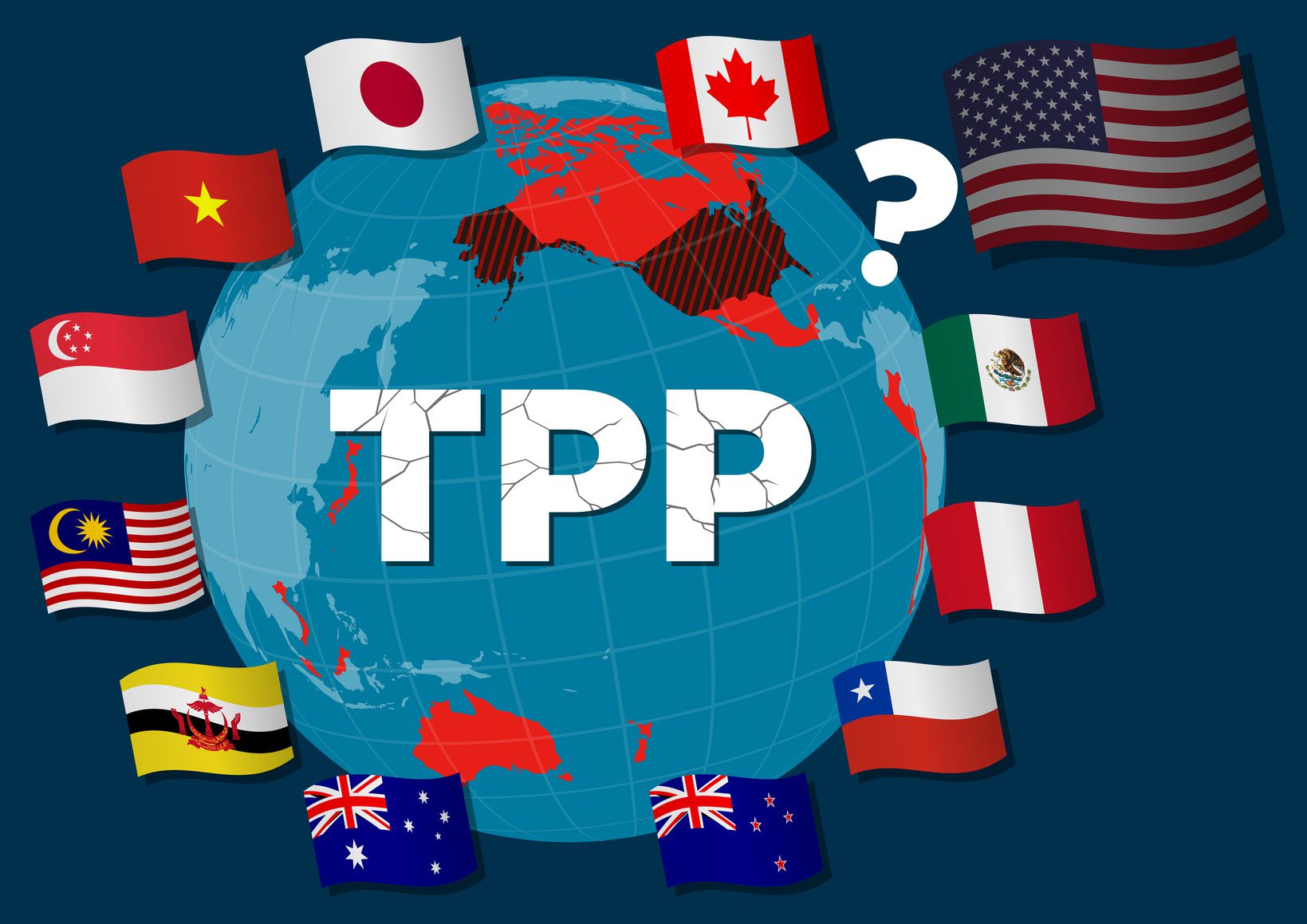

The Trans-Pacific Partnership (TPP) is a regional trade agreement involving twelve countries on the Pacific Rim: Australia, Brunei, Canada, Chile, Japan, Malaysia, Mexico, New Zealand, Peru, Singapore, the USA, and Vietnam. TPP was to be the largest regional trade agreement as the countries involved accounted for 40% of the world’s GDP and 26% of global trade by value. TPP differed from usual trade partnerships as the agreement, along with focus on free trade, also promoted intellectual property protection, enhanced labor standards, and environmental protection, as well as took into account the needs of a digitized global economy – setting new standards for 21st-century global trading environment.

Negotiations on the deal were concluded in October 2015 and representatives from each country signed the agreement in February 2016. TPP was to come in effect after approval of the agreement by each country’s legislature. Before the deal could materialize, the newly elected president of the USA, Donald Trump, issued an executive order in January 2017 withdrawing the country from the process – leaving remaining member-countries in a lurch.

As per the terms, TPP could come in effect only if ratified by six countries accounting for 85% of the group’s total GDP. Since the USA accounted for about 60% of the groups’ total GDP, its withdrawal killed the deal in a literal sense. However, the remaining eleven countries are still clung to the idea of TPP and are reluctant to throw away years of negotiation. This leads to a question – can TPP survive without the USA? We take a look at the countries’ take on a newly proposed TPP agreement involving the group of eleven countries, without the USA.

Japan to lead the pact

When the USA opted out from TPP, the first reaction of the prime minister of Japan reaffirmed that the trade deal was meaningless without participation of the USA – the largest market in the group. Soon Japan realized that even through eleven-member TPP it can still yield net economic gains in medium-sized markets such as Australia and Vietnam. Moreover, this deal was essential to reduce the dominance of China in the region. Since TPP has been an integral part of the Japanese government’s growth strategy, the country took a U-turn from its previous stance and took the lead in pushing forward the relaunch of TPP involving eleven member countries.

Australia, New Zealand, Singapore, and Canada still in favor of the deal

Australia and New Zealand, being advocates of trade liberalization, were among the first few countries to express their intention to continue with TPP without the USA. Through the eleven-country TPP, Australia and New Zealand aim to gain access to new markets such as Canada, Mexico, and Peru, with which these countries do not have any trade agreements. Moreover, New Zealand expects to gain about two thirds of the US$2.7 billion in estimated annual benefits (after 15 years) if the eleven-member TPP is implemented with terms similar to original deal. This indicates that TPP would result in net economic benefit for the members even without participation of the USA.

Singapore, being an export-oriented economy, strongly favors multilateral trading system especially with like-minded trading partners and thereby the country is likely to support eleven-member TPP.

In a bid to strengthen its economic ties with the pact, especially with Japan, Canada has also shown interest in renegotiating the TPP with remaining eleven countries and urges other nations to join the trade deal.

These countries believe that it would be better to have a weakened TPP without the US participation than to have no TPP at all.

Latin countries sense distinct opportunity

Mexico has enjoyed free access to markets of its largest trading partners – the USA and Canada – since 1994 through North American Free Trade Agreement (NAFTA). As Trump administration turns unfriendly and hostile towards Mexico, threatening to renegotiate or even withdraw from NAFTA, Mexico is looking to diversify its trading options to counter the effect. Under such circumstances, Mexico is more than willing to pursue an eleven-member TPP that will open new markets for the country.

Smaller countries such as Chile and Peru are also keen on going ahead with the proposed eleven-member TPP so as to gain access to Asian markets.

Some Asian countries may lack enough incentive to continue with TPP in absence of the USA

Without participation of the USA, it seems difficult to lure countries such as Malaysia and Vietnam that agreed to change rules on state-owned enterprises and deregulate key sectors such as finance, telecommunications, and retail in anticipation of gaining access to the US market. Both the countries signaled waning enthusiasm for TPP in absence of their largest target market – the USA. For instance, through the twelve-member TPP, Vietnam was expecting its textile exports to increase by 40%, primarily due to free access to the US market at 0% tariff. Thus, without the USA, the expected economic benefits of TPP would drastically reduce for Vietnam as well as Malaysia.

In such a scenario, these countries might give preference to alternative trade agreements such as Regional Comprehensive Economic Partnership (RCEP) that includes seven of the TPP members (i.e. Malaysia, Vietnam, Brunei, Singapore, Japan, Australia, and New Zealand). Launched in 2015 and backed by China, RCEP is the proposed trade agreement aimed to economically integrate 16 countries in Asia and Oceania region, however, this trade deal lacks the elements of intellectual property protection or labor and environment laws that TPP is set apart with. Brunei, the smallest economy in the pact, is actively involved in further discussions, however, its final take on eleven-member TPP is still unclear.

EOS Perspective

While the twelve-member TPP is effectively dead, the new TPP, if at all formed and implemented in future, would be very different from the original one. Being the largest economy in the group, the USA had great negotiation power in development of the original TPP. With the USA’s exit, the power dynamics have changed and the remaining member countries might want to reconsider certain terms that they agreed upon only under the pressure of the USA. For instance, Malaysia could demand change in TPP’s rules that restrict the country to offer preferential treatment to ethnic Malays in government contracts. Such difference in power dynamics might indicate that the eleven-member TPP negotiation process is unlikely to be as simple as just striking ‘the USA’ off the 5,000+ page agreement. It might take years of discussions and renegotiations before the member countries could reach a consensus.

Furthermore, increasing participation from other countries is one way to fill the void left by the USA. TPP members have extended invitation to several countries, including China and UK. China immediately rejected the proposal stating that the TPP is very complex and the country is rather focused on RCEP. In the meantime, UK is yet to confirm its intent. UK is looking to deepen ties with other countries to boost trade after Brexit, thus, joining the TPP might be a good decision, as this might possibly allow the country to have direct access to the markets of the current eleven member countries. However, UK would need to objectively weigh in the estimated benefits of joining TPP as against the stringent requirements of the deal.

At this stage, the future of TPP is uncertain. In the end, all countries act in the best interest of their own economies as well as own political aspirations. Though the ambitious TPP proposal laid out a strong vision for international rules-based trade and investment system for global digital economy, it is far from implementation unless it ensures satisfactory benefits for all the countries involved.