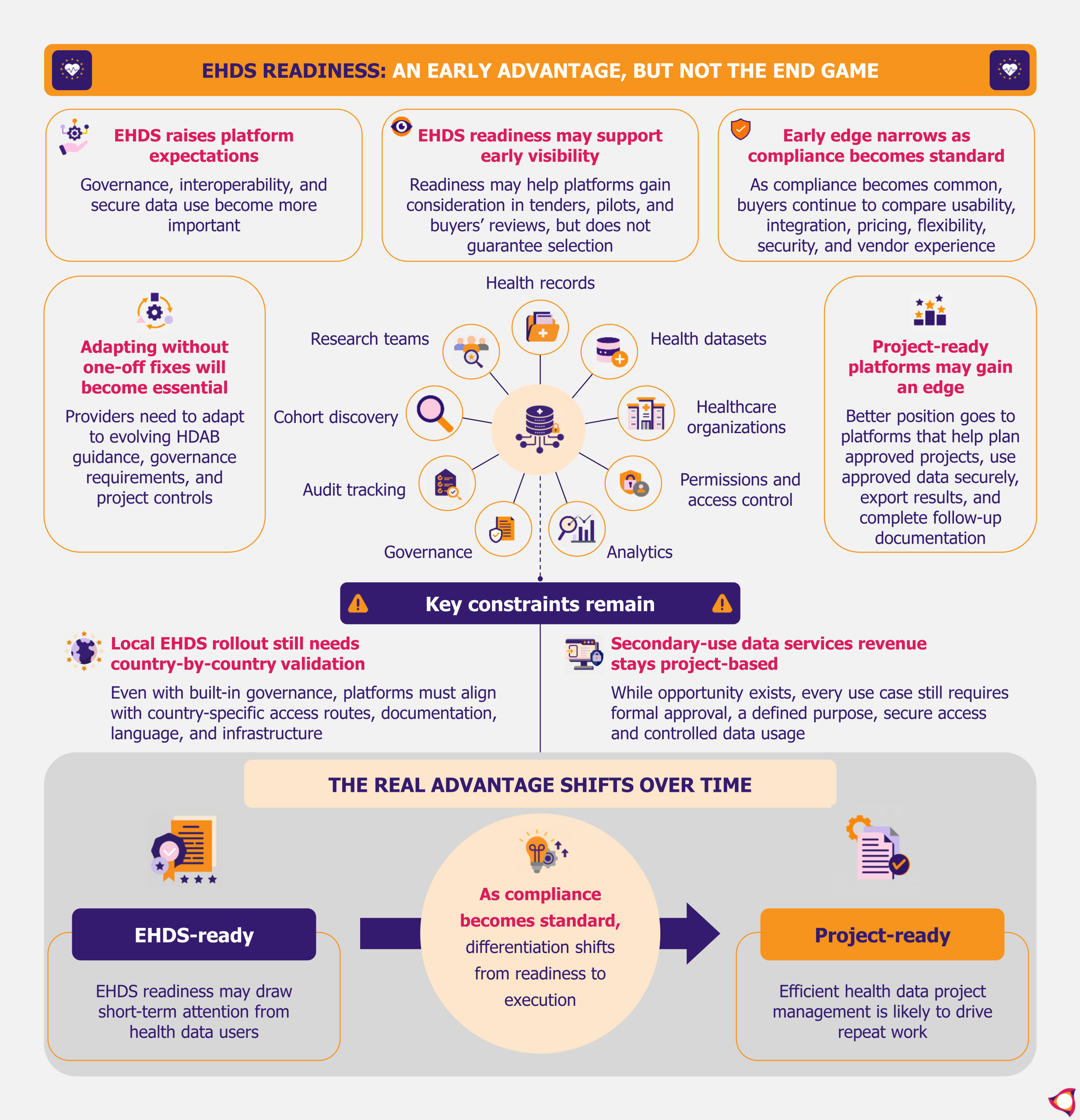

The phased rollout of the European Health Data Space Regulation (EHDS) will likely increase the importance of governance and interoperability. It will also raise expectations around secure data use for health data platforms. Early readiness may help some diagnostic and health data platforms look safer to buyers during the transition period. However, the advantage is likely to be limited, as EHDS compliance will eventually become a basic requirement, and buyers will still judge platforms on integration, usability, and proven deployment.

EHDS readiness may help health data platforms enter buyer reviews

EHDS, the first common EU health data space, entered its transition phase in March 2025. Health data platform providers have since started preparing for stricter governance expectations.

Some providers are already shaping their products and messaging around EHDS-related needs, but they are not all doing it the same way. BC Platforms has positioned its Trusted Research Environment as EHDS-ready, with buyer-facing messaging that emphasizes secure data access, federated analysis, and compliance. Lifebit’s TRE messaging points to a similar need around approved researcher access without moving sensitive data from its source. Better Care brings in another angle, as its shared care records can help structure data from separate systems into a more usable base for exchange.

This approach and EHDS-ready messaging may help these platforms gain greater consideration in tenders, pilots, and buyer reviews. It may also support participation in research data projects. Buyers can ask to see how the platform handles regulated data work, and do not have to rely on a promise that the providers will add these features later. Still, EHDS readiness will not decide selection on its own. Buyers will also look at integration with existing systems, pricing, flexibility, analytics, security, and vendor track record.

Early adoption can help platform providers learn how buyers interpret EHDS requirements before EHDS implementation becomes fully established. It is also likely to expose them earlier to update costs, as standards, buyer expectations, and local rules evolve.

In the long run, as compliance becomes common, this early advantage is likely to shrink. Newer providers may get a small opening if they build around EHDS from the start, but established providers will still benefit from existing integrations, proven deployment, and buyer trust. However, new companies may still struggle with buyer trust, limited real-world experience, brand recognition, and system integration.

EHDS Readiness Gives Health Data Platforms Only a Short Head Start by EOS Implicium

Built-in governance may make local EHDS rollout easier to prove

EHDS sets common rules, but rollout will still happen through national systems, access bodies, and existing health data infrastructure. For these platforms, built-in governance helps only if providers can adapt it to local realities and checks. Buyers need to see how access rules, permissions, restrictions, tracking, sharing rules, and security work inside the product. They need to know what changes for their country, systems, and data-access route.

That gives providers a reusable base, but it does not remove local work. They still need to map the same controls to each country’s access route, HDAB process, dataset catalog, and buyer systems. For buyers, this makes the local rollout discussion more concrete. The provider can adjust an existing setup instead of rebuilding the technical and compliance layer each time.

Expansion across countries will still depend on how easily providers can localize the deployment package. That includes country-specific documentation, language, support materials, and links to national digital health infrastructure. It may also mean reflecting local opt-out choices or patient-access rules where they apply. These are not core product rebuilds, but they still take buyer time and local proof, which can slow rollout even when the platform is technically ready.

Platforms that add governance later face a different problem. They may have to retrofit access controls, audit trails, and secure processing into systems customers already use. They also need to show how these controls work with each country’s HDAB route, permits, and local IT setup. That is harder than adapting a platform that already handles controlled health data use. Buyers will ask for evidence during tenders or public projects, before they choose a vendor. If the provider cannot show this clearly, deployment can slow down or require extra technical work before launch.

EHDS may turn secondary-use health data into project-based revenue

EHDS enables healthcare organizations to use secondary health data for research, training, innovation, and AI development. However, data access is tightly controlled. Health Data Access Bodies (HDABs) grant data access only for authorized purposes. Platform providers do not get free access to this data, but they can sell infrastructure and workflow around approved use. This includes analytics, cohort discovery tools, and federated data access.

For hospitals, research networks, and other data users, the burden is finding relevant datasets and getting approval. They also need a secure place to work with the data, so health data platforms can sell tools and support around those steps, not just analytics alone.

In the near term, EHDS-compliant secondary-use services are likely to sell first through research projects, pilots, and public health data initiatives. Buyers are likely to test them where the data source, permit route, and secure workspace are already clear. Early growth is more likely for platforms with usable datasets, secure workflows, trusted customer relationships, and proof from real projects, not just large data volume.

Related reading:

Denmark’s Digital Health Edge Gives Health Tech Firms Room to Grow

Wider repeatable revenue may come later if platforms can package the repeated work around secondary-use projects. This includes dataset search, HDAB application support, and approved analysis workflows.

Scale will still be limited by the way EHDS access works. Each project may need a defined purpose, approved access, secure processing, and clear limits on how users handle the data. That makes the opportunity useful, but slower and more project-based than a simple software rollout.

EOS Implic-Action: EHDS is set to favor project-ready platforms

EHDS will move through phased implementation, and health data platforms will not all benefit in the same way. Some may support national or large-scale data projects, while others may stay in smaller or more specific projects. Buyers are likely to separate them by capabilities, buyer trust, integration strength, and compliance readiness.

Europe already has strong data protection and security regulations. GDPR and national health data laws mean many platforms are not starting from scratch on privacy, security, and data governance. That helps providers who already work with structured health data or shared care records, especially in more digitally mature markets. They may find it easier to show their readiness because buyers can see they have dealt with regulated health data before.

That only gets providers part of the way. Existing privacy work does not make a platform EHDS-ready, and experience in one country does not prove the same setup will work elsewhere. The stronger position will belong to providers that can show real project experience, not just prior privacy compliance.

Phased rollout may give small providers time to prepare

EHDS implementation will progress in phases. This will give providers more time to plan investment, update systems, and align their capabilities with the evolving requirements. This may help smaller platform providers, but only if they use that time carefully. With fewer resources and smaller compliance teams, they may need to focus first on markets or projects where they can realistically prove readiness.

EHDS rule changes push platforms to update without one-off fixes

EHDS will keep moving from regulation into working procedures as HDAB guidance, secure processing rules, and technical specifications take shape. Platform providers need more than compliance documents. They need a product setup that can absorb new project rules without a rebuild. That means accommodating new permits, workspace limits, user roles, audit records, and output checks as guidance changes. Providers that handle this through normal product updates will have easier buyer reviews. Buyers can see how the platform keeps pace without extra fixes before each project.

As secondary-use projects grow, buyers will also need to know whether a dataset is worth using before they spend time applying for access. EHDS is moving toward dataset quality and utility labels, especially for publicly funded data. Platforms that can show what a dataset covers, where it is weak, and which projects it can support may save buyers from weak applications and poor pilots.

Efficient health data project management is likely to become the real edge

Eventually, simply being EHDS-compliant will not be enough for health data platform providers. EHDS readiness may help platforms get earlier attention during the transition period, but that advantage is likely to narrow once compliance becomes a normal buyer requirement.

Explore more analysis on EOS Implicium

The stronger position will belong to providers that make approved data projects easier to run. Buyers will need help before and after access is granted, including support with project planning, secure analysis, result export, and follow-up documentation. Providers that handle more of this workflow can become harder to replace. They may also win more repeat work from research networks, hospitals, and public data projects.