Chronic wounds such as diabetic foot ulcers, venous leg ulcers, and pressure injuries keep treatment costs high. Healing is slow, treatment is repeated, and patients often need regular clinic or nurse support. That leaves room for therapies that can shorten treatment, cut visits, or move care out of expensive facilities.

Topical oxygen therapy (TOT) falls between two existing options on cost. Hyperbaric oxygen therapy (HBOT) is on the expensive end, since it needs chambers and specialist facilities. Standard dressings are on the cheap end, familiar, and easy to buy. TOT lands in the middle, and patients can use it closer to home without the HBOT setup.

But clinics still use it mainly as an add-on to standard wound care, not as a replacement. To sell beyond early users, vendors have to prove a few things. They need to show which wounds heal faster with it, what work it takes off nurses and clinics, and who pays. They also have to show that staff can set up the device, watch it, and write up the treatment without slowing down the clinic’s work. Until vendors can prove this, TOT stays a niche product.

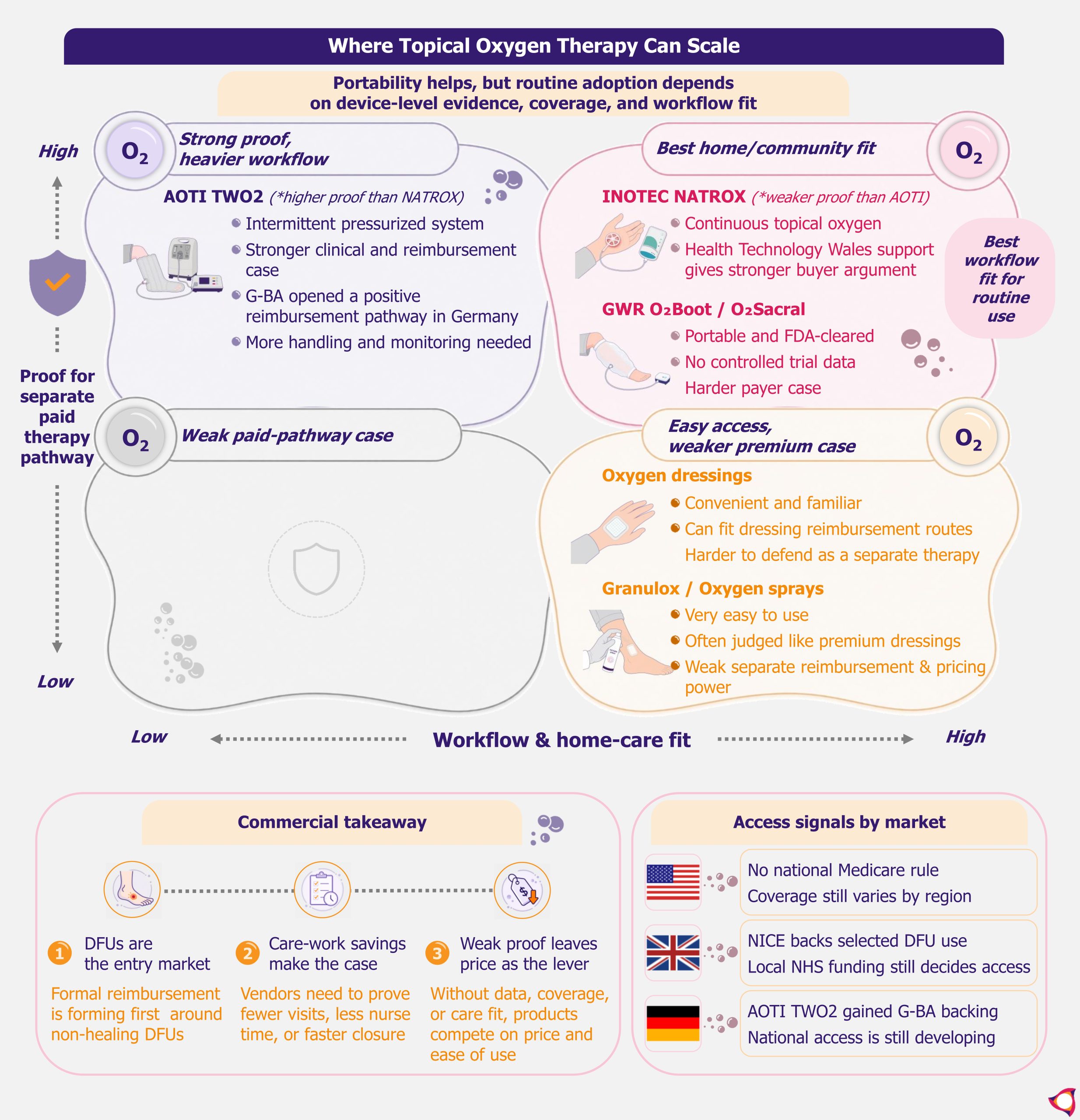

Topical oxygen formats win through different wound care routes

Continuous and low-pressure systems fit home and community care most easily. Inotec’s NATROX is the strongest example in this category. It works best for clinics or payers trying to cut visits, and for programs that identify non-healing diabetic foot ulcer patients early. Health Technology Wales supports the routine adoption of continuous topical oxygen for chronic non-healing and complex diabetic foot ulcers. That gives NATROX a stronger buyer argument than most formats in this group.

GWR Medical’s O2Boot and O2Sacral are also portable, low-pressure devices with FDA clearance. Their clinical evidence is weaker, with no controlled trial data, which limits how far they can go with payers. The broader limit for both is that institutional support is still mainly around defined diabetic foot ulcer groups. Wider wound-care claims need more proof by wound type.

Intermittent pressurized systems, with AOTI’s TWO2 as the main example, can make a stronger reimbursement case in some markets. AOTI’s TWO2 has higher-quality clinical data than most TOT formats, including a double-blinded sham-controlled RCT. That gives TWO2 a clearer path to payer coverage than formats with weaker evidence. But the day-to-day use needs more handling than a plain continuous system. A clinic is unlikely to commit until it sees that the monitoring and patient support fit its existing staff and workflow.

Oxygen sprays risk being priced like premium wound dressings

Mölnlycke’s Granulox and similar hemoglobin oxygen sprays compete for the same wound care budget as TOT devices, but they work differently. They apply hemoglobin to the wound surface to carry ambient oxygen to the tissue, with no device or oxygen source needed. That makes them easier for clinics to try, but it also limits pricing. Some studies show faster closure, fewer dressing changes, and less pain with Granulox. But the evidence comes from small studies, and in most markets it has not been enough to secure a separate budget line.

Oxygen-based dressings are bought and evaluated more like advanced dressings than as a separate therapy. Convenience helps, but buyers will still compare them with standard dressings on price, change frequency, and healing speed. If vendors cannot prove enough of a difference, sprays and oxygen dressings risk being bought as premium dressings rather than as a separately reimbursed therapy.

Topical Oxygen Therapy Needs Payer Oxygen to Scale in Wound Care by EOS Implicium

Device-specific coverage decides which topical oxygen vendors can scale

Topical oxygen has more clinical backing than it used to, but it is still not a default therapy. IWGDF’s 2023 guidelines recommend considering it as an add-on for diabetes-related foot ulcers that are not healing with standard care. The guidelines also assume the clinic has the resources to support treatment.

A category-level recommendation like this helps every vendor equally, so it does not decide which products win. What separates them is local coverage, which each vendor has to secure for its own device. Before clinics use it more widely, vendors have to line up that coverage. They also need to work out which patients qualify and earn a spot in the care pathway.

Lower topical oxygen costs count only when they cut wound care work

Buyers will look at the cost of getting a wound healed, not just the price of the device. TOT costs less to deploy than HBOT because it does not need chambers, specialist facilities, or repeated clinic-based sessions. That comparison only helps for the small group of patients who would otherwise get HBOT.

For most wounds, the real alternative is dressings, so the cost case has to be made against dressings, not against HBOT. The money argument only works if TOT actually cuts costs, through fewer visits, less nurse time, fewer complications, or a shorter course of treatment. If it does not clearly change any of those, the lower device cost will not matter.

HBOT keeps a role where coverage and protocols already support it, especially selected severe or ischemic wounds. In the USA, for example, Medicare covers HBOT for diabetic lower-extremity wounds only under strict conditions. The wound must be due to diabetes, classified as Wagner grade III or higher, and show no measurable healing after at least 30 days of standard wound care. That gives HBOT a clearer paid route in some severe cases, while topical oxygen often has to prove coverage locally.

Dressings keep a low-acuity share because they are familiar, easy to buy, and cheaper upfront. TOT wins only where the extra device cost is tied to faster closure, easier home follow-up, or fewer high-cost visits.

Digital tools such as wound imaging, oxygen sensors, and adherence tracking have a role, but a limited one. They are worth having when they show whether the wound is closing and whether the patient is using the device. They also need to tell the clinic whether it can skip a visit or stop treatment early. When they cannot show those things, they add cost without changing what the buyer decides.

Each wound care buyer needs a different topical oxygen sales case

Specialist wound centers will ask for clinical proof first, but they also need coding, staff fit, and clear patient-selection rules. Payers and home-health providers have different priorities. They need cost comparisons, home-care pilots, and adherence data showing that TOT cuts visits, nurse time, transport, or non-healing weeks.

For most wounds in this group, the realistic alternative is continued dressing treatment, not HBOT, so payers will compare TOT costs against dressings, not against HBOT. Coverage alone is not enough. Vendors also need reimbursement dossiers, clinic training, and patient-selection tools so that buyers can actually act on the coverage that exists.

Underserved markets can generate useful evidence on whether local staff can run the device and whether patients stay on treatment. But they are not automatically high-margin markets, and payers in higher-income countries will not always accept that evidence. Patient populations, care settings, and cost structures differ enough that those payers typically want data from their own markets.

Reimbursement splits where topical oxygen can sell

US topical oxygen coverage stays uneven without a national Medicare rule

Reimbursement is still what divides this market most. In the USA, Medicare has no national rule that directly covers topical oxygen for chronic non-healing wounds. CMS amended its hyperbaric oxygen national coverage determination in 2017 and left coverage of topical oxygen to the Medicare Administrative Contractors region by region.

In December 2024, the DME MACs held a Contractor Advisory Committee meeting to consider revising the relevant LCD to include topical oxygen. No updated LCD had been issued as of early 2026. What a provider can get paid still depends on where they are.

Related reading:

CAMPs Scale-Up Turns Wound Care into a Test of Evidence and Reach

Europe still turns topical oxygen evidence into access locally

The UK is moving, but access is still local. NICE updated NG19 in late 2025 to include topical oxygen as an add-on for diabetic foot ulcers where healing is not progressing. Access still depends on local NHS funding and care-pathway decisions. Wales is further along through Health Technology Wales support for continuous topical oxygen in chronic non-healing and complex diabetic foot ulcers. Vendors can use this as stronger evidence support, but they still need local funding and care-pathway work.

Germany gives AOTI a stronger European proof point after the G-BA issued a positive reimbursement recommendation for TWO2 for diabetic foot ulcers in June 2025. Full national reimbursement was not yet in place as of early 2026, with formal guidelines still in development.

Vendors that can show local clinical data, support the reimbursement process, and work with in-country partners will move from evidence to sales faster than those that cannot.

Private-pay markets keep topical oxygen use narrow

In lower- and middle-income markets, TOT will likely reach patients first through private wound clinics, hospital partnerships, or home-health networks. In these channels, payment does not depend on public reimbursement. These channels can charge patients directly for the therapy, include it in a broader treatment fee, or split the cost across a care package.

Broader use will be harder in rural or lower-income segments. TOT needs staff to set up the device, monitor it, and document treatment, and thinly staffed clinics often cannot do that. Patients in these segments also tend to choose the lower upfront cost, which favors dressings. Without reimbursement or public purchasing, dressings will keep share even when healing takes longer.

EOS Implic-Action: Paid DFU pathways will widen the vendor gap

The non-healing diabetic foot ulcer segment is where formal reimbursement pathways are forming first, and that is where vendors should concentrate their evidence and market access work. Payers respond to cost arguments, not device price alone, and home and community delivery is where those cost savings are easiest to demonstrate.

The market is already splitting. AOTI and NATROX are building reimbursement track records, and the gap with the rest of the field is widening. Products without comparable data, coverage, or a home-care workflow are unlikely to follow that path. For those, the more likely outcome is competing on price and ease of use, which limits margin and clinical positioning.

Winning a pathway slot requires more than clinical data. Clinics need to know which patients to select, how to document progress for payment, and when to stop treatment. Vendors that supply those tools alongside the device are easier to adopt into a standard workflow. Those that do not are harder to use routinely, even when the clinical case is accepted. That is a practical barrier that data alone does not remove.

Skin substitute price cuts give US topical oxygen vendors an opening

TOT is not the only therapy competing for non-healing DFU patients. Skin substitutes target the same population and have had established Medicare reimbursement for longer. That reimbursement is now being restructured. In December 2025, CMS withdrew new LCDs for skin substitutes that would have tightened coverage. At the same time, it cut the payment rate to a flat US$127.14 per square centimeter. Coverage rules stayed in place, but the payment cut reduced the economics of that category.

Explore more analysis on EOS Implicium

TOT vendors pursuing CMS coverage are therefore entering a market where the main competing adjunct therapy is under pricing pressure it was not facing two years ago. That benefits AOTI most directly, since it is already in the CMS process and has the data to support a coverage case. Vendors that have built their business in Europe do not have the US reimbursement groundwork in place to act on this opening. Their better route is to keep winning coverage country by country in Europe, where their data and partners already are.